324 KiB

Instant commission payouts fintech thesis (Brazil focus)

Session ID: ses_2f39164d0ffend7HDsg8OkqEbd Created: 3/20/2026, 6:07:48 PM Updated: 3/20/2026, 6:26:13 PM

User

Looking at this @session-ses_2fe5.md Does a company like this exist?

Assistant (Plan · gpt-5.4 · 15.8s)

Thinking:

Analyzing company existence

The user is asking about the company based on a specific file they provided. We need to analyze whether such a company exists, and it’s likely I’ll need to do some research using webfetch or GitHub for context. I think adjacent companies may be out there, but the exact match might not exist. Since traditional search engines might not be an option here, I could explore navigating with a browser for broader research.

Thinking:

Exploring company research

I think I need to use webfetch on company websites I already know from the file, like DailyPay, Caju, and Xerpay. The user’s asking if companies like these exist, so I’ll need to assess if there are companies combining commission payouts with instant access, wallets/cards, and analytics. From what I recall, adjacent companies may exist, such as Clair or Rain. I’ll confirm names and specifics using webfetch and possibly explore further with a research task. A well-researched plan is essential!

Thinking:

Considering research options

The user has asked a direct question, so I think I can provide an answer. It might be helpful to do some research using webfetch or a search engine if needed. I should avoid asking the user unnecessary questions. I also need to think about context management, ensuring the conversation stays concise since I only plan to use one tool. It might be wise to check the file for mentions of comparable companies, specifically around line 688. I could answer based on my knowledge that while similar pieces exist, an exact end-to-end solution may not.

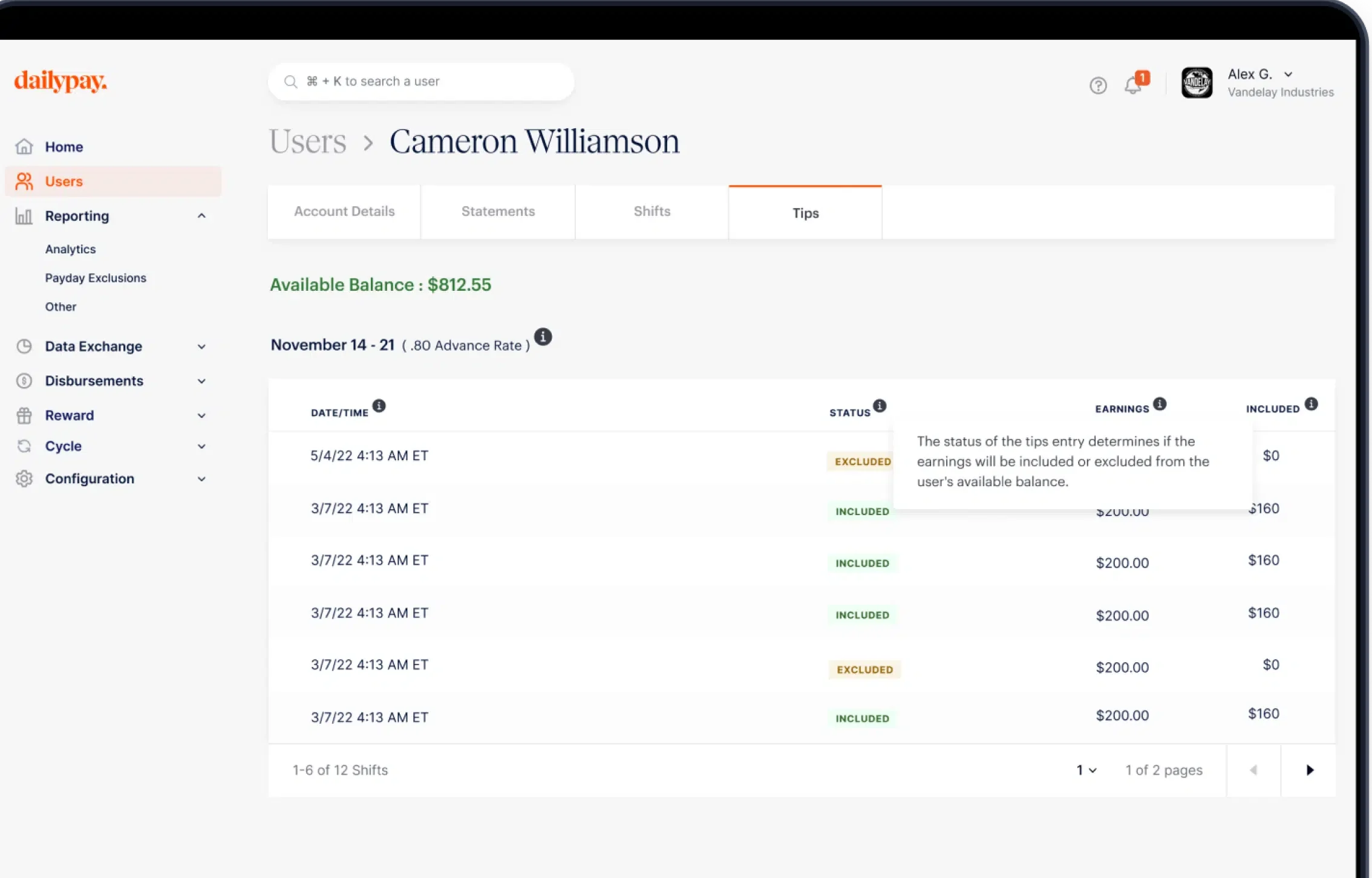

Tool: webfetch

Input:

{

"url": "https://www.dailypay.com/",

"format": "markdown",

"timeout": 20

}

Output:

On-Demand Pay Platform - DailyPay

[Skip to main content](#content)

Are you an employee? [Log in or sign up](https://dailypay.app.link/WaMojfWFLTb)

[Skip to main content](#content)

[](/)

[](/)

- Employers

[

DailyPay Overview

On-Demand Pay — also known as earned wage access — gives employees access to their earned pay before payday. DailyPay is your key to improving recruitment, retention, motivation and productivity.

](/earned-wage-access-platform/)[

Why DailyPay

When your employees have greater control over their finances, your business wins too.

](/benefits/)[

Clients

DailyPay partners with industry leaders across HCM and payroll for a seamless experience.

](/clients/)[

Integrations

DailyPay integrates with 180+ HCM, payroll and time management systems to deliver industry-leading EWA to millions of users.

](/integrations/)

Industries

[

Overview

While each industry has to deal with unique economic factors and different customer bases, one constant is the employee. Learn how to support them with On-Demand Pay.

](/industries/)

- [Hospitals & Healthcare](/industries/healthcare/)

- [Grocers & Supermarkets](/industries/grocers-supermarkets/)

- [Retail](/industries/retail/)

- [Call & Contact Centers](/industries/call-contact-centers/)

- [Restaurants & QSR](/industries/qsr-restaurants/)

- [Manufacturing](/industries/manufacturing/)

- [Travel & Hospitality](/industries/travel-hospitality/)

- [Public Sector](/industries/public-sector/)

- [Franchise](/industries/franchise/)

See the DailyPay difference [Let's Talk](/demo/)

Featured resources

[

Education Series

All You Need to Know About On-Demand Pay

](/on-demand-pay/)

[

Case Study

DailyPay: The Benefit Duracell’s Employees Asked for by Name

](/resource-center/case-studies/duracell-benefit-employees-asked-for/)

[

Case Study

Offering DailyPay Helped Adecco Improve Retention in the Staffing Industry

](/resource-center/case-studies/adecco-standing-out-in-the-staffing-industry-with-dailypay/)

- Solutions

Platform & Features

[ DailyPay Platform

Industry-leading On-Demand Pay.](/earned-wage-access-platform/) [ Small Business New

On-Demand Pay for businesses under 500 employees.](/on-demand-pay-small-business/)

[ DailyPay Visa® Prepaid Card

Reach even more employees with On-Demand Pay.](/dailypay-card/) [ Cycle

Easily disburse off-cycle pay.](/cycle/) [ Tips

Real-time digital tips access.](/real-time-digital-tips-access-platform/) [ Perks New

Employ financial benefits with curated discounts and deals on life’s biggest expenses](/perks/)

By initiative

[

Implement On-Demand Pay

On-Demand Pay improves employee retention and recruitment.

](/earned-wage-access/)

[

Reduce Employee Turnover

How much does turnover cost your company?

](/resource-center/employee-turnover/)

[

Improve Employee Financial Wellness

How does employee financial wellness impact your bottom line?

](/resource-center/employee-financial-wellness/)

[

Improve Employee Retention

Experience cost savings and higher workplace morale.

](/resource-center/employee-retention/)

[

Increase Employee Engagement

Boost productivity and revenue.

](/employee-engagement-strategies/)

[Explore all Integrations](/integrations/) Our On-Demand Pay solution integrates with payroll and time management systems.

Featured resources

[

Turnover Calculator

How much is turnover costing your company?

](/employee-turnover-calculator/)

[

whitepaper

DailyPay Tops List as #1 Adopted Financial Wellness Benefit

](/surveys/top-financial-wellness-benefit/)

[

Thought Leadership

How Can an On-Demand Pay Platform Help Your Business?

](/earned-wage-access/)

- Our Partners

[

Partners Overview

Work with DailyPay to implement the most trusted solutions in On-Demand Pay that work best for your clients and their employees.

](/marketplace/)

[

Human Capital Management

](/marketplace/#ct-tabs)

[

Workforce Management

](/marketplace/#ct-tabs)

[

Banks & Financial Institutions

](/marketplace/#ct-tabs)

[

DailyPay Built InTM New

The easiest way for HCM partners to integrate EWA into their platform.

](/marketplace/ewa-payroll-builtin/)

Featured Partner

[

DailyPay: The Preferred On-Demand Pay Solution for Workday Customers

](/workday/)

- Resources

Learn

[

Blog

](/resource-center/blog/)[

Case Studies

](/resource-center/case-studies/)[

Guides

](/resource-center/ebooks/)[

Podcasts

](/resource-center/podcasts/)[

Webinars

](/resource-center/webinars/)

[ On-Demand Pay Education Series

Learn how to get started with On-Demand Pay.](/on-demand-pay/) [ DailyPay Certification Program

Free courses to earn EWA certification & SHRM credit.](/certification-program/)

Company

- [About Us](/about-us/)

- [Impact](/impact/)

- [Awards & Recognition](/awards/)

- [Press Center](/press-center/)

[Resource Center](/resource-center/) Our library of On-Demand Pay thought leadership.

Featured resources

[

Turnover Calculator

How much is turnover costing your company?

](/employee-turnover-calculator/)

[

Blog

How Employee Engagement Impacts Your Bottom Line

](/resource-center/blog/the-three-levels-of-employee-engagement-and-how-they-impact-your-bottom-line/)

[

Blog

What is a Paycheck Advance and Why You Should Avoid Them

](/resource-center/blog/the-three-levels-of-employee-engagement-and-how-they-impact-your-bottom-line/)

- [For Employees](https://get.dailypay.com/?utm_source=wwwheader&utm_medium=crossdomain)

### For Employees

Ready to see your available balance?

[Log In](https://dailypay.app.link/wpRH63ZlyTb) [Sign Up](https://dailypay.app.link/vYyj0iSlyTb)

[Get a Demo](/demo/)

Search Icon A magnifying glass representing search

[](/)

Search

Close Search Popup Close the search popup

popular searches

[earned wage access](/?s=earned+wage+access) [On-Demand Pay](/?s=On-Demand+Pay) [improve employee retention](/?s=improve+employee+retention) [employee financial wellness](/?s=employee+financial+wellness) [reduce turnover](/?s=reduce+turnover) [Increase employee engagement](/?s=Increase+employee+engagement)

[Log In](https://app.dailypay.com/login?utm_source=wwwlogin&utm_medium=crossdomain) [Get a Demo](/demo/)

Modern HCM and payroll providers thrive on DailyPay partnerships. [Learn More](/marketplace/)

# Hard Work

Pays

Off

On the Daily

Pay Your Employees On Their Schedule With On-Demand Pay

DailyPay provides an industry-leading On-Demand Pay platform that gives your employees access to their pay when they want it.

[Get a Demo](/demo/)

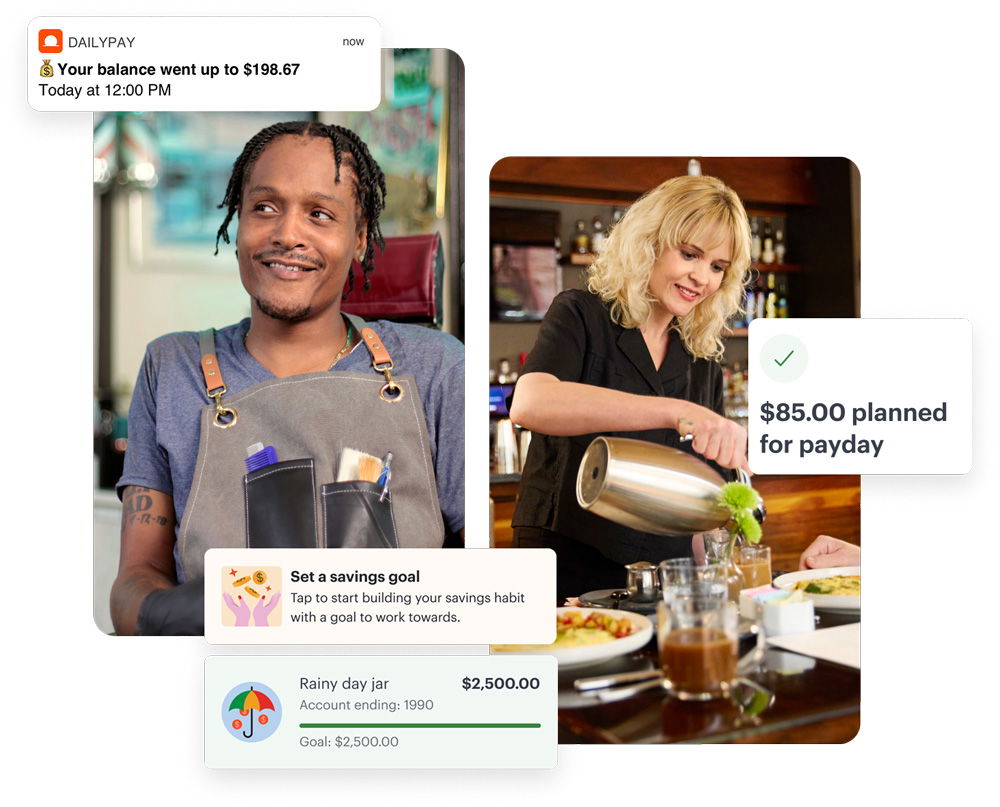

[DailyPay’s Platform](/earned-wage-access-platform/ ) helps employers recruit, retain, and engage employees. In turn, employees can build, earn, and grow their wealth. We are transforming how the world gets paid so every worker can meet life’s moments with confidence.

[Explore Platform](/overview/)

Trusted by leading companies

integration partners

## Recruit, Retain,

and Engage Employees

DailyPay transforms employers into industry leaders by revolutionizing the way employees access their pay.

[See how we stand out](/benefits/)

[](https://iframe.mediadelivery.net/embed/208304/c33bf779-e863-45e3-963d-143df312a8b6?autoplay=true&loop=true&muted=true&preload=true&responsive=true)

### Help Them Build, Earn, and Grow Their Wealth

DailyPay’s financial wellness empowers employees to take control of their earnings.

[See how it works for employees](https://get.dailypay.com/)

## Recognized as the Industry Leader

We’re proud to have been honored with the following [awards](/awards/).

successful implementation

## Commitment to Employee Adoption

The DailyPay Solution starts by seamlessly and securely integrating with payroll systems to leave little to no added work for payroll teams. From there, collaborative services work with you on technical implementation, customized launch strategy, employee activation, client onboarding, training, marketing and more.

**Simple Implementation**

**No building or retooling**

**Ready fast**

## The Insights You Need, When You Need Them

Read about the latest research, events and more involving DailyPay and On-Demand Pay and how we’re working to build a path towards modern pay solutions for all.

[Explore all resources](/resource-center/)

[

DailyPay Selected as Workday's Strategic Partner for On-Demand Pay

The companies are now offering a more connected experience for joint customers that empowers employees with access to their earnings on their own schedule, when they need it most. The Strategic Partnership will help companies recruit, retain, and engage employees.

Learn more

](/press-center/press-releases/workday-and-dailypay-form-strategic-partnership-to-bring-on-demand-pay-to/)

## Latest

[

Report

**DailyPay Tops List as #1 Adopted Financial Wellness Benefit**

](/surveys/top-financial-wellness-benefit/)

[

Blog

**How Improved Financial Wellness Can Help Employers**

](https://www.dailypay.com/resource-center/blog/improve-employee-financial-wellness/)

[

BLOG

**Empower Your Workforce With Real-Time Digital Access Through DailyPay Tips**

](https://www.dailypay.com/resource-center/blog/how-restaurants-can-instantly-disburse-tips-in-real-time/)

[

BLOG

**The Hidden Benefits of On-Demand Pay for Employers**

](https://www.dailypay.com/resource-center/blog/hidden-benefits-of-on-demand-pay-employers/)

[

Blog

**How Financial Wellness Improves Employee Engagement**

](https://www.dailypay.com/resource-center/blog/financial-wellness/)

[

BLOG

**Attract and Retain the Next Generation of Government Workers With Financial Wellness Benefits**

](https://www.dailypay.com/resource-center/blog/attract-public-sector-employees-ewa/)

### Business Leaders Count On DailyPay

“As a result of implementing DailyPay, we now have 58% less turnover in the first two weeks on the job among our agents who are using DailyPay compared to those who are not using DailyPay.”

Rob Schultz

SVP of HR & Compliance for DialAmerica

[Read the case study](https://www.dailypay.com/resource-center/case-studies/case-study-dialamerica/)

### Business Leaders Count On DailyPay

“We implemented DailyPay and saw a 25% increase in operating hours… we’re starting not only to see it stabilize, but improve.”

Darin Harris

CEO of Jack in the Box

[Read the case study](https://www.fool.com/earnings/call-transcripts/2021/11/23/jack-in-the-box-inc-jack-q4-2021-earnings-call-tra/)

### Business Leaders Count On DailyPay

“These efforts have resulted in better seasonal hiring results, which was one of our main goals in rolling out this program. We have also seen an increase in retention rates, with turnover currently at 36% for non-DailyPay users and 22% for DailyPay users.”

Dawn Ehrhart

SVP of Shared Service Operations for the Americas for The Adecco Group

[Read the case study](https://www.dailypay.com/resource-center/case-studies/adecco-standing-out-in-the-staffing-industry-with-dailypay/)

### Business Leaders Count On DailyPay

“Statistics show that 52% of our associates who use DailyPay use it for bills, 13% use it for transit and 8% use it for food.”

Jake Bell

CEO of Christian Horizons

[Read the case study](https://www.dailypay.com/resource-center/case-studies/dailypay-and-christian-horizons-a-strong-partnership-through-times-of-crisis/)

### Business Leaders Count On DailyPay

“We couldn’t be happier with the team we work with at DailyPay. Their people are their true differentiator against other On-Demand Pay providers.”

Taylor Leevers

Special Projects Manager for Leevers Supermarkets, Inc.

[Read the case study](https://www.dailypay.com/resource-center/case-studies/dailypay-leevers-supermarkets-partners/)

## See Why Top Companies Choose DailyPay

[Let's Talk](/demo/)

**Empowering for Employees**

Greater financial control with access to up to 100% of their DailyPay Balance to meet the challenges of unexpected financial disruptions.

---

Improved planning with visibility to withdrawals and earned pay in one easy-to-use app.

---

No need for a pre-existing checking or savings account.

**Simple and Secure for Employers**

No change to payroll processes — DailyPay compliantly handles it all.

---

Seamless integration with HCM, payroll, banking and benefit applications.

---

Enterprise-grade platform that keeps data private and the service running so it's always there when your employees need it.

[](/)

DailyPay HQ

55 Water Street New York, NY 10041

[Contact us](/contact/)

- [](https://www.glassdoor.com/Overview/Working-at-DailyPay-EI_IE1197210.11,19.htm)

- [](https://www.facebook.com/dailypay)

- [](https://twitter.com/dailypay)

- [](https://www.linkedin.com/company/dailypay/)

- [](https://www.instagram.com/dailypay/)

- [](https://www.youtube.com/channel/UCOHcuqx2v4Yqpm1bdt1AMWA)

- ##### Company

- ##### Company 1

- [About Us](/about-us/)

- [Awards & Recognition](/awards/)

- [Impact](/impact/)

- [Security](/security/)

- [Compliance](/en-us/legal/compliance/)

- [Press Center](/press-center/)

- [Careers](/careers)

- [DailyPay Pioneers](/pioneers/)

- ##### For Employers

- [Overview](/overview/)

- [Why DailyPay](/benefits/)

- [Clients](/clients/)

- [Industries](/industries/)

- [Channel Partners](/marketplace/)

- [Integrations](/integrations//)

- ##### Platform & Features

- [DailyPay Platform](/earned-wage-access-platform/)

- [DailyPay Visa® Prepaid Card](/dailypay-card/)

- [Cycle](/cycle/)

- [Reward](/reward/)

- [Tips](/real-time-digital-tips-access-platform/)

- ##### Resources

- [Blog](/resource-center/blog/)

- [On-Demand Pay Education Series](/on-demand-pay/)

- [Employee Turnover Calculator](/employee-turnover-calculator/)

- [Integrations](/integrations/)

- [Employee Retention](/resource-center/employee-retention/)

- [On-Demand Pay](/resource-center/how-can-earned-wage-access-help-your-business/)

- [Resource Center](/resource-center/)

- [Research & Statistics](/stats/)

- [For Employees](https://get.dailypay.com/?utm_source=wwwfooter&utm_medium=crossdomain)

EN

- [English (EN)](https://dailypay.ca/en-ca/)

- [Français (FR)](https://dailypay.ca/fr-ca/)

---

- [English (EN)](https://dailypay.co.uk)

---

- [English (EN)](https://dailypay.com)

For Employees

[

visit get.dailypay.com

](https://get.dailypay.com/?utm_source=wwwfooter&utm_medium=crossdomain)

Get the DailyPay app

[](https://apps.apple.com/us/app/dailypay-on-demand-pay/id1399085077)[](https://play.google.com/store/apps/details?id=com.DailyPay.DailyPay&hl=en_CA&gl=US)

[](/)

- [](https://www.glassdoor.com/Overview/Working-at-DailyPay-EI_IE1197210.11,19.htm)

- [](https://www.facebook.com/dailypay)

- [](https://twitter.com/dailypay)

- [](https://www.linkedin.com/company/dailypay-inc/)

- [](https://www.instagram.com/dailypay/)

- [](https://www.youtube.com/channel/UCOHcuqx2v4Yqpm1bdt1AMWA)

- [© DailyPay 2026](/)

- [Privacy](/en-us/legal/privacy/)

- [Do Not Sell or Share My Personal Information](/legal/cookie-declaration/)

- [Consumer Privacy Notice](https://assets.dailypay.com/wp-content/uploads/dailypay-glba-consumer-notice.pdf)

- [Accessibility](/accessibility/)

- [Terms of Service](/en-us/legal/terms-of-service/)

- [OSS Attribution](/legal/open-source-software-attribution)

- [Program Terms](/en-us/legal/program-terms/)

- [Status](https://status.dailypay.com/)

App Store, Apple Pay, and the Apple Logo are trademarks of Apple Inc. Google, Google Play, and Google Pay are trademarks of Google LLC. Samsung Pay is a registered trademark of Samsung Electronics Co., Ltd. All other trademarks shown are the property of their respective owners.

The DailyPay Visa® Prepaid Card is issued by The Bancorp Bank, N.A., Member FDIC, pursuant to a license from Visa U.S.A. Inc. and can be used everywhere Visa debit cards are accepted.

Your funds are FDIC insured through The Bancorp Bank, N.A., Member FDIC. DailyPay is not FDIC-insured. Deposit insurance coverage only protects against failure of The Bancorp Bank, N.A.

For residents in the state of Connecticut, these services may be restricted or unavailable due to restrictions in your state on earned wage access. Please see this [Help Center](https://help.dailypay.com/hc/en-us/articles/23630960763411-I-live-in-CT-How-do-I-use-DailyPay?utm_source=Iterable&utm_medium=email&utm_campaign=DPC_DPC_Inactive%252FPost_Term_-_BF%252FCM_S%2526amp%253BG_-_Email_2_-_111524.html_-12345) article for further information.

DailyPay, LLC's Earned Wage License Number in Nevada is EWA00004.

DailyPay, LLC's Earned Wage License Number in Wisconsin is 2587396EWA.

DailyPay, LLC's [NMLS](https://www.nmlsconsumeraccess.org/) ID is 2587396.

### Evaluating On-Demand Pay Vendors?

Learn the basics of On-Demand Pay, how to evaluate potential vendors, and the On-Demand Pay features your company needs to ensure success.

Download the Guide

## Subscribe Form

Please tell us a little bit about yourself, so we know who and where to send our eBook to.

Cancel

### Thank You!

Check your email in the next few minutes for our eBook, **On-Demand Pay 101**.

Tool: webfetch

Input:

{

"url": "https://www.branchapp.com/",

"format": "markdown",

"timeout": 20

}

Output:

Fast Payments for Any Workforce | Branch

[](/)

Solutions

[

Pay Your Way

](/solutions/pay-your-way)

[

Branch App & Card

](/solutions/branch-app-and-card)

[

Branch Direct

](/solutions/branch-direct)

[

Embedded Finance

](/solutions/branch-embedded-finance)

[

Custom Branded Solutions

](/solutions/custom-branded-solutions)

industries

[

Healthcare

](/industry/healthcare)

[

Hospitality

](/industry/hospitality)

[

Gig Platforms & Marketplaces

](/industry/gig-platforms-marketplaces)

[

Logistics & Transportation

](/industry/logistics-transportation)

[

Business Services

](/industry/business-services)

[

Construction & Energy

](/industry/construction)

[

Agriculture

](/industry/agriculture)

use cases

[

Cashless Tips & Mileage

](/use-cases/cashless-tips-mileage)

[

Earned Wage Access

](/use-cases/earned-wage-access)

[

Financial Wellness

](/use-cases/financial-wellness-tools)

[

Paycard & Direct Deposit

](/use-cases/paycard-direct-deposit)

[

1099 Independent Contractor Payouts

](/use-cases/1099-independent-contractor-payouts)

[

W-2 Employee Payments

](/use-cases/w-2-employee-payments)

resources

[

All Resources

](/resources)

[

Blog

](/blog)

[

Books & Guides

](/resources?type=Books+%26+Guides)

[

Reports & Data

](/resources?type=Reports)

[

Case Studies

](/case-studies)

company

[

About Branch

](/about)

[

Contact

](/contact)

[

Jobs

](https://job-boards.greenhouse.io/branch)

[

News

](/news)

[Integrations](/integrations)

[Start Today](/demo)[How It Works](/solutions/pay-your-way)

# Fueling the Future of Workforce Payments

Branch delivers faster, more flexible options for businesses to pay their workers, empowering people with easy access to earnings and tools to build financial freedom.

[Start Today](/demo)[How It Works](/solutions/pay-your-way)

Trusted by

## Branch Works for You

Explore all the ways our award-winning, end-to-end platform helps you and your workers thrive.

## Simple Setup, Instant Access

Whether you’re looking to launch a turnkey or customized payments experience, we’ve got a solution that meets your needs.

[Get a Demo](/demo)

Easy to Launch

Easy to set up, no matter your technical skills or timeline. Start sending money to your team on day one—no large deposits or pre-funding required.

Seamless Integrations

We can work with all kinds of HCM, payroll, tax, and time & attendance systems. [Check out integrations](/integrations)

Customizable Options

From ready-to-use payout solutions to custom branded payment experiences, choose from a variety of options to suit your needs.

Available for Free

Branch is available at no cost to companies and offers free options for workers. Earners that sign up with Branch can receive a free bank account, fast access to earnings, and personal finance tools to help set long-term goals.

## Improve Hiring & Productivity

Faster payouts can attract top talent and keep workers coming back for their next shift.

### 83%

of employees believe they should be able to access their pay each day [\[source\]](https://www.forbes.com/sites/edwardsegal/2021/09/13/most-workers-want-to-be-paid-automatically-every-day-according-to-new-poll/?sh=11d12037293f)

### 1 in 3

individuals claim financial stress has negatively impacted workplace productivity [\[source\]](https://www.forbes.com/sites/edwardsegal/2021/09/13/most-workers-want-to-be-paid-automatically-every-day-according-to-new-poll/?sh=11d12037293f)

### 2.5x

increase in applicants when on-demand pay was added to the job description \[Branch customer survey\]

### 86%

felt more incentivized to work when on-demand pay was offered \[Branch customer survey\]

## Industries That Trust Branch

Branch simplifies payments and helps businesses thrive across a spectrum of industries.

[

Healthcare

](/industry/healthcare)

[

Hospitality

](/industry/hospitality)[

Logistics & Transportation

](/industry/logistics-transportation)

[

Business Services

](/industry/business-services)[

Gig Platforms & Marketplaces

](/industry/gig-platforms-marketplaces)

## What Our Customers Are Saying

From time and money saved to reduced staff turnover, Branch has made an impact for businesses of all sizes.

Manna

“The number one question that our applicants ask—especially younger applicants—is whether or not we have earned wage access. You will knock yourself out of the game if you’re not offering that to your employees.”

Mary Lazzaroni

,

VP of Human Resources

Read their story

[](/case-studies/manna)

Hop City Craft Beer & Wine

“It speeds things up a lot. On a Friday night, the manager is responsible for paying out the whole staff at the end of the night… that is time-consuming, just the physical manual labor. I’d say it saves between 1-2 hours of management time each day. Now the process takes 10 minutes, tops.”

CJ Dimino

,

Director of Restaurant Operations

Read their story

[](/case-studies/hop-city)

StaffHealth

“Same-day pay has been the #1 tool in reducing the level of no-call, no-shows we experience”

Anthony Miller

,

Director of Operations

Read their story

[](/case-studies/staffhealth)

Servicon

"In the past, many employees had to use payday lenders and similar entities for loans with interest rates that are sky high. Branch gives them the best option for getting cash at zero cost to them."

Liliana Monter, a Payroll Manager

,

Read their story

[](/case-studies/servicon)

Three15

“I had an initial phone call and I think we were live a couple hours later. We ended up getting everyone paid with Branch that day.”

Mandy Moseley

,

Owner, Three15 Studios

Read their story

[](/case-studies/three15)

## Latest Insights

Explore the future of work and payments

[More Insights](/blog)

[

Hiring on Demand: How Staffing Firms Can Win with Event-Driven Demand

Read more

](/blog/hiring-on-demand-how-staffing-firms-can-win)

[

From Cash Tips to Digital Wallets: The Evolution of Tipping and What It Means for Operators

Read more

](/blog/from-cash-tips-to-digital-wallets-the-evolution-of-tipping)

[

Defining Success in the Trades: How to Improve Subcontractor Satisfaction in Construction

Read more

](/blog/how-to-improve-subcontractor-satisfaction-in-construction)

## Unlock a Happier, More Productive Workforce

[Start using Branch today](/demo)

[](/)

Branch delivers faster, more flexible options for people to get paid.

[

](https://www.facebook.com/branch/)[

](https://www.instagram.com/branch.app/)[

](https://x.com/branch)[

](https://www.linkedin.com/company/branch-app/)

Solutions

- [Pay Your Way](/solutions/pay-your-way)

- [Branch App & Card](/solutions/branch-app-and-card)

- [Branch Direct](/solutions/branch-direct)

- [Embedded Finance](/solutions/branch-embedded-finance)

- [Custom Branded Solutions](/solutions/custom-branded-solutions)

Industries

- [Healthcare](/industry/healthcare)

- [Hospitality](/industry/hospitality)

- [Gig Platforms & Marketplaces](/industry/gig-platforms-marketplaces)

- [Logistics & Transportation](/industry/logistics-transportation)

- [Business Services](/industry/business-services)

- [Construction](/industry/construction)

Use Cases

- [Cashless Tips & Mileage](/use-cases/cashless-tips-mileage)

- [Earned Wage Access](/use-cases/earned-wage-access)

- [Financial Wellness](/use-cases/financial-wellness-tools)

- [Paycard & Direct Deposit](/use-cases/paycard-direct-deposit)

- [1099 Independent Contractor Payouts](/use-cases/1099-independent-contractor-payouts)

- [W-2 Employee Payments](/use-cases/w-2-employee-payments)

Resources

- [All Resources](/resources)

- [Blog](/blog)

- [Books & Guides](/resources?type=Books+%26+Guides)

- [Reports & Data](/resources?type=Reports)

- [Case Studies](/case-studies)

Company

- [Integrations](/integrations)

- [About Branch](/about)

- [Contact](/contact)

- [Jobs](https://job-boards.greenhouse.io/branch)

- [News](/news)

Help

- [Terms](/legal/start)

- [App Support](https://support.branchapp.com/hc/en-us)

- [Admin Login](https://payadmin.branchapp.com/login)

- [Security Portal](https://security.branchapp.com/)

- [Your Privacy Options](#)

© Branch

2026

- All Rights Reserved

Branch is not a bank. Banking services are provided by Evolve Bank & Trust, Member FDIC or Lead Bank, Member FDIC (“Sponsor Banks”), as listed on the back of a user's Branch Card. FDIC insurance only applies for eligible accounts should the Sponsor Bank holding the user's funds fail. The Branch Mastercard Debit Card is issued by the Sponsor Bank pursuant to a license from Mastercard and may be used everywhere Mastercard debit cards are accepted.

### Your Privacy Options

We use cookies to provide you with the best possible experience. They also allow us to analyze user behavior in order to constantly improve the website for you.

[See our Cookie Policy](/cookie-policy)

Reject all

Cookie choices

Accept All

Functionality

Analytics Storage

Ad Storage

Ad User Data

Ad Personalisation

Personalization Storage

Security Storage

Thank you! Your submission has been received!

Oops! Something went wrong while submitting the form.

Accept selection

Tool: webfetch

Input:

{

"url": "https://www.captivateiq.com/",

"format": "markdown",

"timeout": 20

}

Output:

Sales Commission Management Software | CaptivateIQ

Javascript must be enabled for the correct page display

Captivate26 is coming to Austin. Join revenue, finance, and comp leaders for real, hands-on conversations. [Register today](/captivate-26)

[](#)

[.svg)](/)

[Why CaptivateIQ](/why-captivateiq)

Products

[Back to Menu](#)[Product](#)

Product

[

CaptivateIQ Incentives

Automate commissions and deliver a better Return on Incentives.

](/incentives)[

CaptivateIQ Planning

Simplify sales planning and maximize territory effectiveness.

](/planning)[

CaptivateIQ Catalyst

Advanced modeling layer for planning and incentives with predictive ML.

](/catalyst)

Platform Capabilities

[

Data Integrations

](/all-integrations)[

SmartGrid™: ELT & Calculation Engine

](/smartgrid)[

Assist: AI-Powered Intelligence

](/assist)[

Enterprise Workflow Automation

](/enterprise-workflow-automation)

Use Cases

- [

Incentive Compensation Management

](/incentives)

- [

Capacity Planning

](/sales-capacity-planning)

- [

Quota Setting

](/quota-setting)

- [

Territory Management

](/territory-planning)

- [

Predictive Modeling

](/catalyst)

- [

Bonuses & MBO Management

](/bonuses)

See for yourself with a product tour

[SPM](https://captivateiq.navattic.com/73c405je)

Solutions

[Back to Menu](#)

for your organization

[

Enterprise

](/enterprise)[

Mid-Market

](/midmarket)[Partners](/partners)[Security & Privacy](/trust)[SOX Compliance](/sox)

for your role

[

Compensation Professionals

](/compensation-manager)[

Finance & Accounting

](/finance-accounting)[

Sales & Revenue Operations

](/revenue-operations)[

Sales Management

](/sales-management)

for your industry

- [

Financial Services

](/financial-services)

- [

Manufacturing

](/manufacturing)

- [

Media & Entertainment

](/media-entertainment)

- [

Medical Devices

](/medical-device)

- [

Retail & Wholesale

](/retail-wholesale)

- [

Technology

](/technology)

Resources

[Back to Menu](#)

EXPLORE COMPANY

[

About CaptivateIQ

The modern sales commission solution to 10x revenue performance.

](/about-us)

- [Careers](/careers)

- [Contact Us](/contact)

LearnING RESOURCES

- [

Customers

Explore how our customers are running commissions with ease and confidence.

](/customers)

- [

Resources

Discover best practices, research reports, and expert guides to supercharge your success.

](/resources)

- [

Events

Register for upcoming events featuring captivating guest speakers, or catch up on-demand.

](/events)

- [

Blog

Unlock the latest insights and best practices on ICM trends and beyond.

](/blog)

- [

ROI Calculator

Calculate your potential ROI with CaptivateIQ.

](/roi-calculator)

[

Explore our new thought leadership hub for all things incentive compensation management

See what's new

](https://multiplier.captivateiq.com/)

[Pricing](/pricing)

- [Login](https://app.captivateiq.com/login)

- [Book a Meeting](https://www.captivateiq.com/request-demo)

[

Opener

](#)

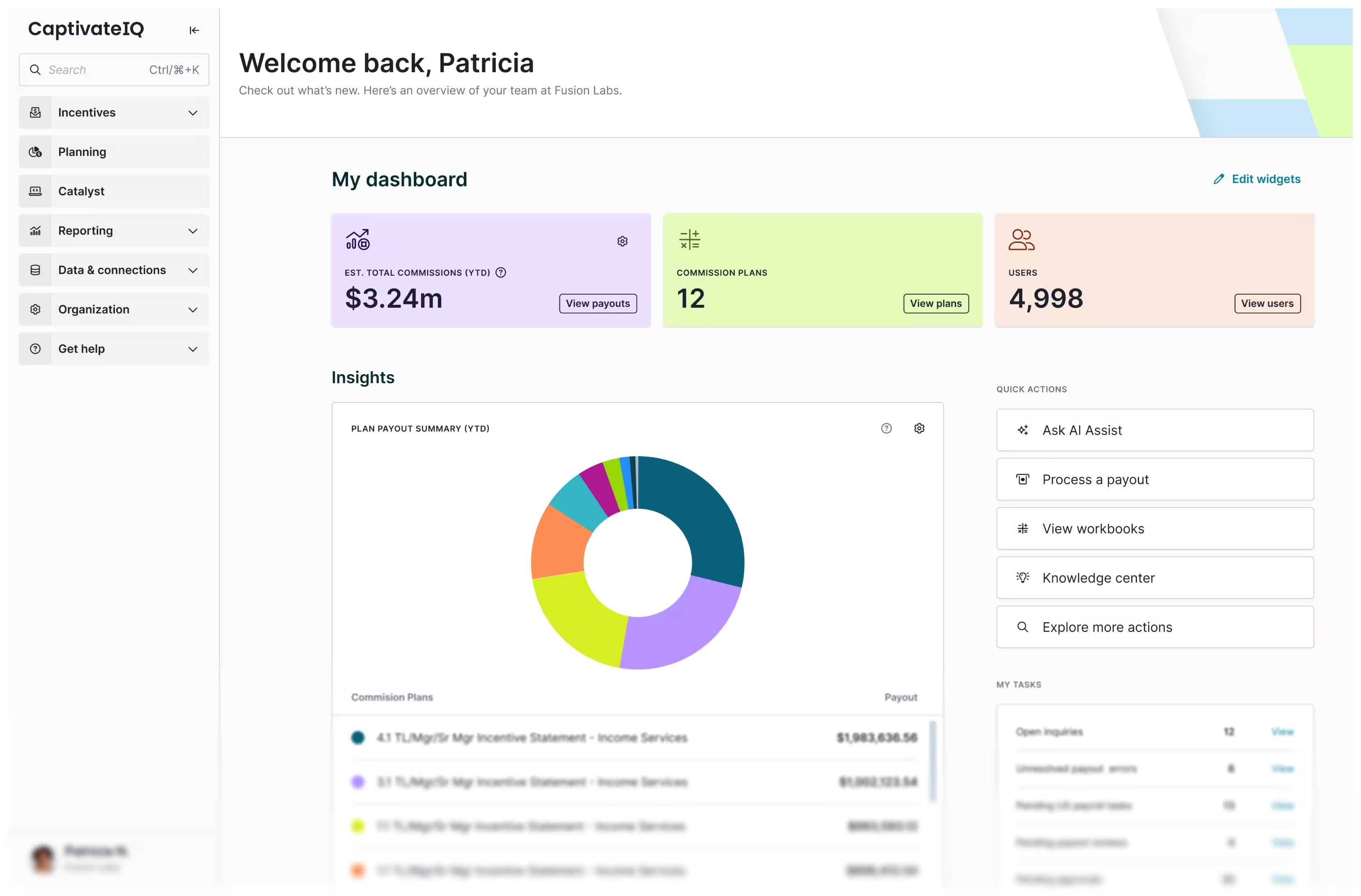

# Planning and incentives in sync.

Finally.

Bring capacity, quotas, territories, and incentives together in a single AI-infused workspace built for agility, alignment, and scale.

[Book a Meeting](#)[Tour the Product](https://www.captivateiq.com/product-tour-general-overview)

[

](#)

Trusted by 800+ companies to chart the path to resilient revenue

Planning & Incentives

Built to

adapt.

## One AI-infused platform

from planning to payout.

From setting objectives to calculating payouts, everything you need to plan, execute, monitor, and adapt tightly integrated sales and incentive compensation strategy. All without relying on services or IT.

SmartGrid ELT

Work off a single source of truth for incentives and planning. Ingest data from any source and transform it in real-time with the SmartGrid ELT modeling engine. Ensuring every model and calculation is built off a clean, up to date dataset.

[Explore this Capability](/smartgrid)

Incentive Compensation Management

Automate commission calculations with precision and transparency. Build any commission plan, give payees real-time visibility into earnings and ensure your incentives are driving desired outcomes.

[Explore this Capability](/incentives)

Sales Capacity and Quota Planning

Balance workloads and ramp times while ensuring quotas are both achievable and aligned with business goals. Compare scenarios to get the right people in seat to hit targets.

[Explore this Capability](/quota-setting)

Territory Management

Build and manage territories that drive results. Automatically assign accounts, optimize opportunities across reps, and adapt boundaries as your business evolves—all with clear alignment across sales and operations.

[Explore this Capability](/territory-planning)

Reporting & Analytics

Turn planning and incentives data into actionable insights. Track performance trends, identify top performers, and understand what drives results with advanced reporting and real-time dashboards that inform strategic decisions.

[Explore this Capability](/product/captivate)

Predictive Modeling

Forecast outcomes before they happen. Use ML-powered models to score accounts, predict quota attainment and identify payout anomalies based on historical performance and trends.

[Explore this Capability](/catalyst)

Assist AI

Build faster, with confidence. Quickly troubleshoot formulas, search documentation, optimize plans and improve payee visibility with natural language queries and intelligent suggestions.

[Explore this Capability](/assist)

## Revenue resilience,

delivered.

You need strategy that grows stronger when things change. That's revenue resilience, and it's built into CaptivateIQ.

[Explore our ROI Calculator](/roi-calculator)

10%

increase in seller attainment

6x

faster plan creation

47%

faster commissions process

9.5%

increase in seller attainment

## CaptivateIQ

is built for agility.

Legacy tools weren’t designed for speed or adaptability. We built CaptivateIQ to make incentive compensation management and planning painless and wildly effective.

[Book a Meeting](#)

Connected workspace

## One source of truth

from capacity planning to payouts

- Clean, up-to-date dataset powered by SmartGrid

- Connected modeling across planning and incentives

- Single source-of-truth across finance, sales ops and compensation

- Real-time commission visibility for payees and leadership

Unbeatable flexibility

## Plan for anything, pivot anytime

- Logic-based workbooks handle compensation plan complexity with ease

- No-code calculation engine to build & adapt without services

- Guided plan-building and scenario modeling with AI Assist

Intelligent optimization

## Make better decisions, faster

- Real-time scenario modeling for planning & incentives

- End-to-end reporting out of the box

- Custom predictive ML models including forecasting and anomaly detection

## Helping operations teams

run smarter and move faster.

Michael D.

Director of Revenue Operations

“Through its flexibility, transparency and automation, CaptivateIQ has become an essential partner in scaling revenue operations for our fast-growing sales organization.”

60x

faster at calculating monthly commissions

[Read their story](/customers/gong)

Brian D.

Director of Sales Finance

"The downstream effects were significant. We were spending so much time on administrative tasks that we couldn’t focus on the real business problems that we wanted to be solving."

60

hours saved per month

[Read their story](/customers/tipalti)

Alex W.

Senior Variable Compensation Analyst

“The additional time \[from CaptivateIQ\] frees up space for analysis … it means I can ensure that our commission plans are really designed to be aligned with our company goals.”

2 days

to roll out new plans

[Read their story](#)

## Complexity,

meet simplicity.

No more crashing Excel files or unmet promises from professional services. Tackle even the most complex sales and compensation plans with speed and confidence.

[Explore Enterprise](/enterprise)[Tour the Product](https://www.captivateiq.com/product-tour-general-overview)

### Scale with SmartGrid

Having firsthand experience with the pain of commissions, our founders built a modern modeling experience. With our SmartGrid™ ELT & calculation engine, you can model plans and calculate commissions at scale.

### Get up and running - fast

Quickly model and test incentives, capacity, territories and quota in real-time without breaking the bank. Launch in as little as two weeks to three months.

### Stay in the driver’s seat

CaptivateIQ’s no-code platform pairs flexibility with ease of use for all your incentive and planning needs. Create reports, test plan changes, and manage incentive compensation with just a few clicks — no technical expertise necessary.

### Comprehensive security and compliance

Protecting your sensitive data is our top priority. Our compliance program meets industry-leading information security standards, undergoing annual independent audits for SOC 1 and SOC 2 compliance.

## We built it because we lived it. Now we’re sharing what we know.

CaptivateIQ started when a few ops leaders hit their limit with broken corp spreadsheets and legacy tools. Now, we help hundreds of companies build better plans, pay accurate commissions, and grow with confidence. Explore insights from the front lines of compensation and planning.

[Learn More](/why-captivateiq)

## Frequently asked questions

[

How does CaptivateIQ automate commissions?

](#)

CaptivateIQ automates commissions by pulling actual sales data from connected CRM systems, applying custom compensation rules to each deal, and generating real-time payout statements. Commission plans are defined using a visual modeling engine called SmartGrid and stay continuously in sync with closed revenue as data updates.

Plans can include:

- Tiers and accelerators

- Bonuses and SPIFs

- Draw structures

- Eligibility rules

SmartGrid handles these structures at scale, so teams can update logic, test scenarios, and maintain accuracy as plans evolve.

[

Why do 800+ companies use CaptivateIQ for Sales Planning & Incentive Management?

](#)

Over 800 companies use CaptivateIQ to manage sales planning and incentive compensation because the platform supports complex plans with high accuracy, flexibility, and transparency. CaptivateIQ replaces manual spreadsheets and rigid legacy tools with automated calculations, real-time visibility, and scalable governance across sales organizations.

[

What’s the advantage of using CaptivateIQ?

](#)

The primary advantage of using CaptivateIQ is the ability to manage complex compensation and planning workflows without heavy IT involvement. The platform combines flexibility, automation, and auditability to support accurate payouts and confident decision-making at scale.

[

What makes CaptivateIQ's incentive management unique?

](#)

CaptivateIQ’s incentive management is unique because it allows compensation logic to be modeled visually while maintaining full traceability from source data to payout. This approach enables rapid plan changes without sacrificing accuracy or control.

[

How does CaptivateIQ ensure data security?

](#)

CaptivateIQ ensures data security through enterprise-grade controls including SOC 2 compliance, encryption at rest and in transit, and role-based access permissions. These safeguards protect sensitive sales, compensation, and employee data across the platform.

[

How is CaptivateIQ's pricing structured?

](#)

CaptivateIQ pricing is structured based on the number of payees, compensation complexity, and required integrations. Pricing is typically tailored to the scope and requirements of each organization’s sales compensation programs.

[

What are the benefits of real-time reports?

](#)

Real-time reports provide immediate visibility into performance, attainment, and expected payouts as sales activity occurs. This visibility helps organizations identify issues earlier and make faster, more informed planning and compensation decisions.

[

Does CaptivateIQ integrate with CRM and payroll systems?

](#)

Yes. CaptivateIQ integrates with Salesforce, HubSpot, NetSuite, Workday, and other source systems to automate data flow and reduce manual work. APIs and data import options allow additional customization. More information on integrations can be found [here](/all-integrations).

[

How does CaptivateIQ ensure data security?

](#)

CaptivateIQ ensures data security through enterprise-grade controls including SOC 2 compliance, encryption at rest and in transit, and role-based access permissions. Customer data is isolated and protected to meet enterprise security requirements.

[

How is CaptivateIQ priced?

](#)

CaptivateIQ pricing is based on company size, compensation complexity, and the modules in use, such as commissions and sales planning. Pricing is typically customized to align with organizational requirements.

[

Why do companies choose CaptivateIQ over other sales compensation tools?

](#)

Companies choose CaptivateIQ for its flexibility, accuracy, and ability to support complex compensation plans without heavy IT dependency. The platform enables rapid plan changes while maintaining transparency and control at scale. Learn how top enterprise businesses have decreased the time they spend on commissions by 75% [here](/customers).

## Join the 800 companies building resilient revenue

with CaptivateIQ

[Book a Meeting](#)

### Let’s customize your demo, takes 30 seconds.

See how top teams automate commissions.

[](#)

Take a quick tour of CaptivateIQ.

Experience the #1 software for Sales and Incentive Planning through a quick self-guided tour.

[Tour the product](https://capture.navattic.com/split/cmhaypgjc01r7la04wh9re1ci)

Sign up for our newsletter

to get the latest ICM insights and best practices

By clicking “Sign Up”, you acknowledge CaptivateIQ’s [Privacy Policy](/privacy-policy).

[Product](#)

- [Assist](/assist)

- [Automate Commissions](/product/automate)

- [Bonuses & MBOs](/bonuses)

- [Captivate with Insights](/product/captivate)

- [Enterprise Workflow Automation](/enterprise-workflow-automation)

- [Incentives](/incentives)

- [Integrations](/all-integrations)

- [Motivate Seller Performance](/product/motivate)

- [Planning](/planning)

- [Platform Overview](/platform)

- [Pricing](/pricing)

- [Product Tour: Incentives](https://captivateiq.navattic.com/695l0e0h)

- [Product Tour: Planning](https://captivateiq.navattic.com/9t10i64)

- [SmartGrid™](/smartgrid)

- [Guided Plan Builder](/guided-plan-builder)

- [Why CaptivateIQ?](/why-captivateiq)

[Solutions](#)

- [Compensation Manager](/compensation-manager)

- [Enterprise](/enterprise)

- [Finance & Accounting](/finance-accounting)

- [Financial Services](/financial-services)

- [Mid-Market](/midmarket)

- [Manufacturing](/manufacturing)

- [Media & Entertainmet](/media-entertainment)

- [Medical Device](/medical-device)

- [Operations](/revenue-operations)

- [Partners](/partners)

- [Retail & Wholesale](/retail-wholesale)

- [Sales Leader](/sales-management)

- [Technology](/technology)

[Legal, Privacy & Security](#)

- [Legal Overview](/legal-overview)

- [Security & Privacy](/security-policy)

- [SOX Compliance](/sox)

[Resources](#)

- [Benchmarking & Market Trends](/resources)

- [Blog](/blog)

- [Customers](/customers)

- [Events](/events)

- [The Multiplier](https://multiplier.captivateiq.com/)

[Company](#)

- [About CaptivateIQ](/about-us)

- [Careers](/careers)

- [Contact](/contact)

[Compare](#)

- [Sales Compensation Software Reviews](https://www.captivateiq.com/explainer/sales-compensation-software-reviews)

- [vs. CallidusCloud](/comparison/callidus)

- [vs. Everstage](/comparison/everstage)

- [vs. Performio](/comparison/performio)

- [vs. QuotaPath](/comparison/quotapath)

- [vs. Spiff](/comparison/spiff)

- [vs. Varicent](/comparison/varicent)

- [vs. Xactly](/comparison/xactly)

[Explainers](#)

- [ASC 606](https://www.captivateiq.com/explainer/asc-606-revenue-recognition)

- [Commission Automation Software](https://www.captivateiq.com/explainer/commission-automation-software)

- [Commission Tracking Software](https://www.captivateiq.com/explainer/commission-tracker)

- [Compensation Management Software](https://www.captivateiq.com/explainer/compensation-management)

- [Incentive Compensation Management Software](https://www.captivateiq.com/explainer/incentive-compensation-management)

- [Sales Commission Calculator](https://www.captivateiq.com/explainer/sales-commission-calculator)

- [Sales Commission Reporting Software](https://www.captivateiq.com/explainer/reporting)

- [Sales Commission Software](http://www.captivateiq.com/explainer/sales-commission-software)

- [Sales Management Software](https://www.captivateiq.com/explainer/sales-software)

- [Sales Performance Management Software](https://www.captivateiq.com/explainer/sales-performance-management)

- [Sales Planning Software](https://www.captivateiq.com/explainer/sales-planning-software)

- [Territory Management Software](https://www.captivateiq.com/explainer/territory-management-software)

© CaptivateIQ, Inc. All rights reserved. Various trademarks held by their respective owners. Featured users may have been compensated; opinions are their own. Customer experiences may vary.

- [Privacy Policy](/privacy-policy)

- [CA Privacy Notice](https://www.captivateiq.com/privacy-policy#california)

-  Your Privacy Choices

- [Sitemap](/sitemap)

Forrester does not endorse any company, product, brand, or service included in its research publications and does not advise any person to select the products or services of any company or brand based on the ratings included in such publications. Information is based on the best available resources. Opinions reflect judgment at the time and are subject to change. For more information, read more about Forrester’s objectivity [here](https://www.forrester.com/about-us/objectivity/).

Gartner® and Peer Insights™ are trademarks of Gartner, Inc. and/or its affiliates. All rights reserved. Gartner Peer Insights content consists of the opinions of individual end users based on their own experiences, and should not be construed as statements of fact, nor do they represent the views of Gartner or its affiliates. Gartner does not endorse any vendor, product or service depicted in this content nor makes any warranties, expressed or implied, with respect to this content, about its accuracy or completeness, including any warranties of merchantability or fitness for a particular purpose.

Tool: webfetch

Input:

{

"url": "https://www.caju.com.br/",

"format": "markdown",

"timeout": 20

}

Output:

Caju • Facilite o seu dia a dia e transforme a experiência dos seus colaboradores

[](/)

Plataforma

O essencial

[

Benefícios

](/plataforma/beneficios)[

Bem-estar e saúde

](/plataforma/saude-e-bem-estar)[

Premiação

](/plataforma/premiacoes)[

Despesas

](/plataforma/despesas)[

Pessoas

](/plataforma/pessoas)

Especiais

[

Promoção Benefícios + Wellhub

](https://produtos.caju.com.br/caju-wellhub-promo%C3%A7%C3%A3o?utm_source=site&utm_medium=referral&utm_campaign=site&utm_term=home&utm_content=menu)[](https://produtos.caju.com.br/seguranca-juridica-2?utm_source=Site&utm_medium=referral&utm_campaign=seguranca_juridica&utm_content=menu_site)

Soluções

Por segmentos

[

Indústria

](/solucoes/industria)[

Serviços

](/solucoes/servicos)[

Tecnologia

](/solucoes/tecnologia)[

Varejo

](/solucoes/varejo)

Por tamanho

[

Pequenas empresas

](/solucoes/pequenas-empresas)[

Médias empresas

](/solucoes/medias-empresas)[

Grandes empresas

](/solucoes/grandes-empresas)

[

Planos

](/planos)

A Caju

Sobre nós

[

A Caju

](/a-caju/a-caju)[

Blog

](https://blog.caju.com.br/?_gl=1*1xtcxy6*_ga*MjA3MDg3ODIxNS4xNzMwNzUzMTA0*_ga_3RPJSREWE0*czE3NjAwMjE0MTkkbzIwMSRnMCR0MTc2MDAyMTQyNSRqNTQkbDAkaDA.)[

Materiais ricos

](https://produtos.caju.com.br/materiais-gratuitos)[

Cajuína

](https://cajuina.org/?_gl=1*1xtcxy6*_ga*MjA3MDg3ODIxNS4xNzMwNzUzMTA0*_ga_3RPJSREWE0*czE3NjAwMjE0MTkkbzIwMSRnMCR0MTc2MDAyMTQyNSRqNTQkbDAkaDA)[

Revenda Caju

](/revenda-caju)[

Cultura e Carreira

](/cultura-e-carreira)

Contato

[

Central de ajuda

](https://ajuda.caju.com.br/s/)[

Fale conosco

](/a-caju/fale-conosco)

Segurança

[

Segurança e certificados

](/a-caju/seguranca-e-certificados)

[

](#)[

Login

](https://auth.caju.com.br/realms/caju/protocol/openid-connect/auth?client_id=sponsor-app&redirect_uri=https%3A%2F%2Fempresa.caju.com.br%2Flogin%2F%23%3F&state=f5f2b387-3a63-4e60-80ea-2cb90a7d33ca&response_mode=fragment&response_type=code&scope=openid&nonce=1c44eb22-cd7d-4dbd-8ece-cc58bcbc0d65&code_challenge=5Lb0J6kMr5CpgFcKu3o5vMip8zSo6ivRbftoGQvvmeo&code_challenge_method=S256)

[Demonstração](https://produtos.caju.com.br/demonstracao-caju-multibeneficios?utm_source=home_site&utm_medium=referral&utm_campaign=demonstracao_caju_multibeneficios&utm_content=header_site&utm_term=botao_header)[Quero Caju](https://quero.caju.com.br/)

[**Mudanças no PAT:** veja o que o novo decreto altera e como manter sua empresa regularizada. **Saiba mais!**](https://produtos.caju.com.br/seguranca-juridica-2?utm_source=Site&utm_medium=referral&utm_campaign=seguranca_juridica&utm_content=faixa_site)

# Facilite o seu dia a dia e transforme a experiência dos seus colaboradores

Da admissão à retenção, centralize benefícios, despesas e gestão de pessoas em uma única plataforma e com taxa zero\*

[

Quero saber mais

](#)

Em breve você receberá as novidade da Caju!

Oops! Something went wrong while submitting the form.

[](https://produtos.caju.com.br/caju-wellhub-promo%C3%A7%C3%A3o?utm_source=site&utm_medium=referral&utm_campaign=site&utm_term=home&utm_content=banner)

+50 mil empresas confiam na Caju

## Centralize benefícios, despesas e pessoas com a Caju

Ganhe agilidade no RH e foco no crescimento da sua empresa.

Benefícios

Gestão simples de benefícios com segurança jurídica garantida.

Controle total do saldo de benefícios CLT, PAT e flexíveis.

[Contrate agora](https://quero.caju.com.br/?utm_source=site&utm_medium=referral&utm_campaign=site&utm_term=botao_contrate&utm_content=despesas)

Despesas

Despesas integradas ao cartão e app Caju, sem complicação.

Unifique reembolsos, adiantamentos e despesas em uma única plataforma.

[Contrate agora](https://quero.caju.com.br/?utm_source=site&utm_medium=referral&utm_campaign=site&utm_term=botao_contrate&utm_content=despesas)

Pessoas

Gerencie toda a jornada do colaborador em um só lugar.

Simplifique processos e traga mais eficiência para o seu RH.

[Contrate agora](https://quero.caju.com.br/?utm_source=site&utm_medium=referral&utm_campaign=site&utm_term=botao_contrate&utm_content=despesas)

## Conheça o plano Essencial

A solução ideal para pequenas e médias empresas: multibenefícios, gestão de despesas e de pessoas em uma única plataforma — tudo integrado, simples de usar e com taxa zero\*.

[Contrate agora](https://quero.caju.com.br/?utm_source=site&utm_medium=referral&utm_campaign=site&utm_term=botao_contrate&utm_content=despesas)

.gif)

## Da pequena empresa à grande corporação, a Caju deixa a rotina mais leve e eficiente

[Fale com um especialista](https://quero.caju.com.br/?utm_source=site&utm_medium=referral&utm_campaign=site&utm_term=botao_contrate&utm_content=despesas)

Pequenas

Tudo que você precisa para organizar seu RH de forma ágil, prática e sem pagar taxa

[Saiba mais >](/solucoes/pequenas-empresas)

Médias

Uma plataforma completa para modernizar o RH e gerenciar toda a jornada do seu colaborador

[Saiba mais >](/solucoes/medias-empresas)

Grandes

Soluções multibenefícios modulares, flexíveis e integradas, do jeito que sua empresa precisa

[Saiba mais >](/solucoes/grandes-empresas)

Pequenas

[Tudo que você precisa para organizar seu RH de forma ágil, prática e sem pagar taxa](#)

[Saiba mais](#)

Médias

[Uma plataforma completa para modernizar o RH e gerenciar toda a jornada do seu colaborador](#)

[Saiba mais](#)

Grandes

[Soluções multibenefícios modulares, flexíveis e integradas, do jeito que sua empresa precisa](#)

[Saiba mais](#)

# Quem escolhe Caju vê resultado!

Menos tempo perdido com burocracia

Mais facilidade para atrair e manter talentos

Colaboradores mais engajados

Quem usa, ama

Para organizações de todos os portes

30%

menos tempo em tarefas operacionais

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

80%

dos clientes dizem que a Caju melhora a atração e retenção de talentos

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

71%

das empresas notam mais engajamento dos colaboradores

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

+1 milhão

de colaboradores com acesso a benefícios que valorizam de verdade

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

+50 mil

empresas simplificam a rotina com Caju

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

Menos tempo perdido com burocracia

30%

menos tempo em tarefas operacionais

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

Mais facilidade para atrair e manter talentos

65%

dos clientes dizem que a Caju melhora a atração e retenção de talentos

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

Colaboradores mais engajados

71%

das empresas notam mais engajamento dos colaboradores

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

Quem usa ama

\+ 1 milhão

de colaboradores com acesso a benefícios que valorizam de verdade

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

Para organizações de todos os portes

\+ 50 mil

empresas simplificam a rotina com Caju

[Contrate agora](https://quero.caju.com.br/?_gl=1*150iziw*_ga*MTAwNjgwMDAyMi4xNzU0MzE1MTU2*_ga_3RPJSREWE0*czE3NjAxMjQ5OTYkbzI2JGcxJHQxNzYwMTI3NTczJGozNSRsMCRoMA..)

## Conheça histórias de quem está colhendo os frutos

[

](#)[

](#)

[

](#)

Joziane Matheus, Coordenadora de RH

“Quando chegou o cartão da Caju com todas essas funções foi uma novidade fantástica, ficamos apaixonados e desde então a gente não tem o que reclamar”

[Ver case completo](#)

[

](#)

Priscila Melo, Analista de RH

“A plataforma da Caju é muito intuitiva e a gente não teve trabalho nenhum, só baixou a planilha, passou os dados e pronto”

[Ver case completo](#)

[

](#)

Elizabeth Jeha, Coordenadora de soluçes

“Com certeza eu recomendo a Caju, como colaboradora e como coordenadora de RH. É realmente um benefício que vem para trazer muitas melhorias para a empresa.”

[Ver case completo](#)

## Soluções que cuidam de quem constrói a sua empresa

Cuidado completo, do trajeto à consulta. Caju facilita o acesso a bem-estar, saúde e transporte para o seu time.

[Fale com um especialista](#)

.gif)

Saúde e bem-estar

Caju conecta sua empresa a serviços de saúde e bem-estar, com gestão simples e uma ampla rede de parceiros.

Mobilidade

Gestão automatizada de vale-transporte e

preço fixo por colaborador.

[Fale com um especialista](https://quero.caju.com.br/?utm_source=site&utm_medium=referral&utm_campaign=site&utm_term=botao_contrate&utm_content=despesas)

## Conheça a Caju na prática!

Assista à nossa demonstração e veja como simplificar a gestão de benefícios e despesas de forma eficiente

[Demonstração](https://produtos.caju.com.br/demonstracao-caju-multibeneficios?utm_source=home_site&utm_medium=referral&utm_campaign=demonstracao_caju_multibeneficios&utm_content=video_bottom&utm_term=cta_video)

[Demonstração](https://produtos.caju.com.br/demonstracao-caju-multibeneficios?utm_source=home_site&utm_medium=referral&utm_campaign=demonstracao_caju_multibeneficios&utm_content=video_bottom&utm_term=cta_video)

## Conheça a Caju na prática!

Assista à nossa demonstração e veja como simplificar a gestão de benefícios e despesas de forma eficiente

[Demonstração](https://produtos.caju.com.br/demonstracao-caju-multibeneficios?utm_source=home_site&utm_medium=referral&utm_campaign=demonstracao_caju_multibeneficios&utm_content=video_bottom&utm_term=cta_video)

[Demonstração](https://produtos.caju.com.br/demonstracao-caju-multibeneficios?utm_source=home_site&utm_medium=referral&utm_campaign=demonstracao_caju_multibeneficios&utm_content=video_bottom&utm_term=cta_video)

O essencial

[Benefícios](/plataforma/beneficios)[Premiação](/plataforma/premiacoes)[Despesas](/plataforma/despesas)[Pessoas](/plataforma/pessoas)

Módulos

[Bem-estar e saúde](/plataforma/saude-e-bem-estar)

Soluções

[Pequenas empresas](/solucoes/pequenas-empresas)[Médias empresas](/solucoes/medias-empresas)[Grandes empresas](/solucoes/grandes-empresas)

Por segmentos

[Indústria](/solucoes/industria)[Serviços](/solucoes/servicos)[Tecnologia](/solucoes/tecnologia)[Varejo](/solucoes/varejo)

A Caju

[Sobre nós](/a-caju/a-caju)[Blog](https://blog.caju.com.br/?_gl=1*1xtcxy6*_ga*MjA3MDg3ODIxNS4xNzMwNzUzMTA0*_ga_3RPJSREWE0*czE3NjAwMjE0MTkkbzIwMSRnMCR0MTc2MDAyMTQyNSRqNTQkbDAkaDA.)[Cajuína](https://cajuina.org/?_gl=1*1xtcxy6*_ga*MjA3MDg3ODIxNS4xNzMwNzUzMTA0*_ga_3RPJSREWE0*czE3NjAwMjE0MTkkbzIwMSRnMCR0MTc2MDAyMTQyNSRqNTQkbDAkaDA)[Histórias de clientes](/a-caju/historias-de-clientes)[Revenda Caju](/revenda-caju)

Pacotes

[Planos e pacotes](/planos)

Para contratar

[quero@caju.com.br](mailto:quero@caju.com.br?subject=Contato%20-%20Site)

Contato

[Central de ajuda](https://ajuda.caju.com.br/s/)[Fale conosco](/a-caju/fale-conosco)[Ouvidoria](/ouvidoria)

Para usuários do app

[oi@caju.com.br](mailto:oi@caju.com.br?subject=Contato%20-%20Site)[Telefone e Whatsapp: (11) 4118-3826](https://api.whatsapp.com/send?phone=551141183826&text=Ol%C3%A1!)

Para empresas

[empresas@caju.com.br](mailto:empresas@caju.com.br?subject=Contato%20-%20Site)[Chat no Portal do RH](https://empresa.caju.com.br/)

Imprensa

[imprensa@caju.com.br](mailto:imprensa@caju.com.br?subject=Contato%20-%20Site)

Segurança e certificações

[Segurança e certificações](/a-caju/seguranca-e-certificados)

Seja um parceiro

[Revenda Caju](/revenda-caju)

Jurídico

[Política de Gestão Integrada de Riscos](/juridico/politica-de-gestao-integrada-de-riscos)

[Portal de privacidade](/juridico/portal-de-privacidade-caju)

[Política de Prevenção à Lavagem de Dinheiro e Combate do Financiamento do Terrorismo (PLD-CFT)](/juridico/pld-cft)

[Política de segurança cibernética](/juridico/politica-de-seguranca-cibernetica)

[Privacidade e segurança](/juridico/privacidade-seguranca)

[Política de privacidade](/juridico/privacidade)

O essencial

[Benefícios](/plataforma/beneficios)[Premiação](/plataforma/premiacoes)[Despesas](/plataforma/despesas)[Pessoas](/plataforma/pessoas)

Módulos

[Bem-estar e saúde](/plataforma/saude-e-bem-estar)

Soluções

[Pequenas empresas](/solucoes/pequenas-empresas)[Médias empresas](/solucoes/medias-empresas)[Grandes empresas](/solucoes/grandes-empresas)

Por segmentos

[Indústria](/solucoes/industria)[Serviços](/solucoes/servicos)[Tecnologia](/solucoes/tecnologia)[Varejo](/solucoes/varejo)

A Caju

[Sobre nós](/a-caju/a-caju)[Blog](https://blog.caju.com.br/?_gl=1*1xtcxy6*_ga*MjA3MDg3ODIxNS4xNzMwNzUzMTA0*_ga_3RPJSREWE0*czE3NjAwMjE0MTkkbzIwMSRnMCR0MTc2MDAyMTQyNSRqNTQkbDAkaDA.)[Cajuína](https://cajuina.org/?_gl=1*1xtcxy6*_ga*MjA3MDg3ODIxNS4xNzMwNzUzMTA0*_ga_3RPJSREWE0*czE3NjAwMjE0MTkkbzIwMSRnMCR0MTc2MDAyMTQyNSRqNTQkbDAkaDA)[Histórias de clientes](/a-caju/historias-de-clientes)[Revenda Caju](/revenda-caju)

Pacotes

[Planos e pacotes](/planos)

Para contratar

[quero@caju.com.br](#)

Contato

[Central de ajuda](#)[Fale conosco](/a-caju/fale-conosco)[Ouvidoria](/ouvidoria)

Para usuários do app

[oi@caju.com.br](mailto:oi@caju.com.br?subject=Contato%20do%20site)[Telefone e Whatsapp: (11) 4118-3826](https://api.whatsapp.com/send?phone=551141183826&text=Ol%C3%A1!)

Para empresas

[empresas@caju.com.br](mailto:empresas@caju.com.br?subject=Contato%20do%20site)[Chat no Portal do RH](https://empresa.caju.com.br/)

Imprensa

[imprensa@caju.com.br](#)

Segurança e certificações

[Segurança e certificações](/a-caju/seguranca-e-certificados)

##### Seja um parceiro

[Revenda Caju](/revenda-caju)

Jurídico

[Aviso de Privacidade para Consignado Privado](/juridico/aviso-de-privacidade-para-consignado-privado)

[Política de Gestão Integrada de Riscos](/juridico/politica-de-gestao-integrada-de-riscos)

[Portal de privacidade](/juridico/portal-de-privacidade-caju)

[Política de Prevenção à Lavagem de Dinheiro e Combate do Financiamento do Terrorismo (PLD-CFT)](/juridico/pld-cft)

[Política de segurança cibernética](/juridico/politica-de-seguranca-cibernetica)

[Termos de uso para empresas](/juridico/termos-de-uso-para-empresas)

[Termos e Condições para Uso do Pix](/juridico/termos-e-condicoes-para-uso-do-pix)

[Privacidade e segurança](/juridico/privacidade-seguranca)

[Política de privacidade](/juridico/privacidade)

[Termos de uso colaboradores](/juridico/termos-de-uso-colaboradores)

\*Oferta válida para empresas que contratarem e utilizarem o produto de multibenefícios da Caju.

[

](https://www.facebook.com/cajubeneficios?_rdc=2&_rdr#)[

](https://www.instagram.com/caju/)[

](https://www.linkedin.com/company/cajubeneficios/)[

](https://www.youtube.com/c/cajubeneficios)[

](https://x.com/cajubeneficios)

##### Baixe nosso app

[](https://apps.apple.com/br/app/caju-benef%C3%ADcios-por-inteiro/id1483671427)[](https://play.google.com/store/apps/details?id=com.caju.employeeApp&hl=pt_BR)

[](/)

CNPJ 33.449.007/0001-44 | Empresa Brasileira de Benefícios e Pagamentos Instituição de Pagamento Ltda

A EBBP IP LTDA ("Caju") é uma Instituição de Pagamento autorizada pelo Banco Central do Brasil e atua como correspondente bancário da VIA CAPITAL - SOCIEDADE DE CRÉDITO DIRETO S.A. ("Celcoin") no produto de Empréstimo Consignado. Como correspondente bancário, a Caju segue as diretrizes da Resolução nº 4.935/21 do Banco Central do Brasil.

Caju® 2026. Todos os direitos reservados

Assistant (Plan · gpt-5.4 · 16.6s)

Thinking:

Evaluating company existence

I need to answer the user's question about whether a specific company exists based on a session file discussing a startup concept. This includes components like payment processing, instant commission payouts, and analytics.

Since there may not be an exact match, I should reference similar companies like DailyPay, Branch, or Caju, especially in Latin America. It could be helpful to search for Brazil-specific examples like Xerpay or SalaryFits to get a clearer idea. If necessary, I might need to gather more information online.

Thinking:

Searching for earned wage access solutions

I want to dig deeper into the web for terms like "earned wage access Brazil" and "instant commissions" to help answer the user’s question about existing companies.

While I might say pieces of this concept do exist, nothing seems to bring together all the components perfectly. I can mention several companies like DailyPay and Branch for earned wage access, or Caju and Creditas Beneficios in Brazil, but there's no exact match for what the user described. I might also reference commission software like “Everstage” or companies that handle commissions in other sectors, hinting at similar models.

Thinking:

Exploring payout platforms

I think I might be getting closer to what the user is looking for with the idea of payouts platforms for marketplaces and direct selling companies that incorporate cards or wallets.

It seems like this could fit into the concept nicely, so I’ll search for relevant solutions or companies that provide these kinds of services. This could help me give a more precise answer for the user about existing options in this space.

Tool: webfetch

Input:

{

"url": "https://www.hyperwallet.com/",

"format": "markdown",

"timeout": 20

}

Output:

PayPal's Global Payout Capabilities | Powered by Hyperwallet

[Skip to content](#content)

Toggle navigation [](/)

- [Documentation](https://portal.hyperwallet.com/docs)

- [Blog](/resources/)

- [Sales](https://www.paypal.com/us/business/contact-sales)

- [Support](/support/)

[](/)

MENUMENU

- [Make Payments](/make-payments/)

- [Features](/features/)

- [Payout Experience](/payout-experience/)

- [Company](/company/)

- [Developers](/developers/)

[

](/resources/developers-product-documentation/venmo-as-a-transfer-method/)[

](/resources/enterprises-payouts/choosing-the-right-payout-methods-for-your-payees/)[](/resources/enterprises-payouts/choosing-the-right-payout-methods-for-your-payees/)[

Which methods suit your business?

](/resources/enterprises-payouts/choosing-the-right-payout-methods-for-your-payees/)[

PAYOUT METHODS

](/resources/enterprises-payouts/choosing-the-right-payout-methods-for-your-payees/)[](/resources/enterprises-payouts/choosing-the-right-payout-methods-for-your-payees/)[CONTACT US](/contact-us/)[LEARN MORE](/make-payments/)

PayPal’s payout capabilities help your organization send mass

payments to contract workers, claimants, freelancers, and

sellers around the world. Leverage Hyperwallet’s full stack

technology to quickly and securely send commissions, rewards,

claims, and rebates to banked and unbanked payees globally.

# PAYOUTS THAT GROW

WITH YOUR BUSINESS

[CONTACT US](/contact-us/)

# SEAMLESSLY

SEND PAYOUTS

## PAYOUTS THAT GROW WITH YOUR BUSINESS

PayPal’s payout capabilities help your organization send mass payments to contract workers, claimants, freelancers, and sellers around the world. Leverage Hyperwallet’s full stack technology to quickly and securely send commissions, rewards, claims, and rebates to banked and unbanked payees globally.

[Learn More](/make-payments/) [Contact Us](/contact-us/)[

PAYOUT METHODS

Which methods suit your business?

](/resources/enterprises-payouts/choosing-the-right-payout-methods-for-your-payees/)

### Solve Payout Problems with Ease

## Payout Capabilities that Help Your Business Succeed

Whether you’re sending payouts to 10 payees or 10,000, PayPal can help you do it quickly, securely, and compliantly. From fast self-serve payouts for small- and medium-sized businesses, to custom configured marketplace and large enterprise integrations, PayPal’s payout capabilities are designed to handle the unique needs of your business – big or small.

[Understand PayPal’s payout capabilities](/make-payments/)

PAYOUT METHODS: Which methods suit your business?

[Click Here](/resources/enterprises-payouts/choosing-the-right-payout-methods-for-your-payees/)

### Global Payout Technology

## Simplify Your Payout Process

PayPal’s payout technology does more than just send payments. Our full stack approach gives organizations of all sizes the payout flexibility and control they need to streamline their operations, scale their business, and delight their payees. [View payout product features >](/features/)

[](/features/)

### Put Your Payees First

## Own the Payout Experience

Create a beautiful user experience for your payees. Highlight your brand, provide a localized UI, and differentiate your enterprise or marketplace from the competition with Hyperwallet’s Pay Portal and Embedded Payout Experiences. [View payout experiences >](/payout-experience/)

[](/payout-experience/)

### PAYOUT DOCUMENTATION

## Explore Our Documentation & Developer Payout Tools

Your developers are already responsible for building your own technology; they shouldn’t have to shoulder the burden of building payout infrastructure too. PayPal’s payout documentation and developer tools are designed to provide stakeholders with the technical and contextual information they need to integrate fast.

[View developer resources](https://docs.hyperwallet.com/content/hyperwallet-payout-documentation)

Streamline your global payouts.

[Contact Sales](/contact-sales/)

#### Get Started

- [Make Payments](/make-payments/)

- [Features](/features/)

- [Payout Experience](/payout-experience/)

- [Company](/company/)

- [Developers](/developers/)

- [Our FX Rates](https://paylution.com/hw2web/consumer/page/currencyCalculator.xhtml)

- [Careers](/careers)

- [Blog](/resources)

#### Support

[Hyperwallet Support Center](/support)

#### Corporate Sales

Canada/US: 1-855-787-1009

Mon-Thu, 9am-8pm / Fri 9am-6pm EST.

Australia: 1-800-729-725

- [GitHub](https://github.com/hyperwallet)

- [Accessibility](/accessibility/)

- [Licenses and Complaints](/state-licenses/)

- [Legal](/legal/)

- [Privacy Policy](/privacy-policy/)

- [Security & Compliance](/security-compliance/)

- [Cookies](#manage-cookies)

©2025 PayPal

Hyperwallet is a member of the PayPal group of companies and provides services globally through its affiliates. These affiliates are regulated in various jurisdictions as follows: In Canada, by PayPal Canada Co., a registered money services business (MSB) within the Financial Transactions and Reports Analysis Centre (FINTRAC) under MSB registration: M19890412, and with Revenu Quebec under MSB license number: 12321. PayPal Canada Co. is a Nova Scotia-incorporated corporation, with its primary business address at 661 University Ave., Suite 506, Toronto, ON M5G 1M1; in the United States, through PayPal, Inc., registered with the US Financial Crimes Enforcement Network and licensed in various U.S. states as a money transmitter, NMLS ID no. 910457, with a principal address at 2211 N. First Street, San Jose, California, 95131; in Australia, through Hyperwallet Systems Australia Pty Ltd, ABN 38 616 937 716, registered with the Australian Securities and Investments Commission, Australian Financial Service Licence no. 499092, with a registered office at Level 24, 1 York Street, Sydney, NSW 2000; in the European Economic Area through PayPal (Europe) S.à r.l. et Cie, S.C.A. (R.C.S. Luxembourg B 118 349), a duly licensed Luxembourg credit institution in the sense of Article 2 of the law of 5 April 1993 on the financial sector, as amended, and under the prudential supervision of the Luxembourg supervisory authority, the Commission de Surveillance du Secteur Financier; In Singapore, through PayPal Pte. Ltd. (UEN: 200509725E), licensed by the Monetary Authority of Singapore as a major payment institution under the Payment Services Act 2019 and with its registered address at 5 Temasek Blvd #09-01, Suntec Tower Five, Singapore 038985; in the United Kingdom, through PayPal UK Ltd, authorised and regulated by the Financial Conduct Authority (FCA) as an electronic money institution under the Electronic Money Regulations 2011 for the issuance of electronic money (firm reference number 994790), in relation to its regulated consumer credit activities under the Financial Services and Markets Act 2000 (firm reference number 996405) and for the provision of Cryptocurrency services under the Money Laundering, Terrorist Financing and Transfer of Funds (Information on the Payer) Regulations 2017 (firm reference number 1000741). Some of PayPal UK Ltd’s products including PayPal Pay in 3 and PayPal Working Capital are not regulated by the FCA.

[](#page-top)

- [Make Payments](/make-payments/)

- [Features](/features/)

- [Payout Experience](/payout-experience/)

- [Company](/company/)

- [Developers](/developers/)

- [Documentation](https://portal.hyperwallet.com/docs)

- [Blog](/resources/)

- [Sales](https://www.paypal.com/us/business/contact-sales)

- [Support](/support/)

Tool: webfetch